United States Sugar Market Size, Share, Trends & Forecast 2033

Market Overview 2025-2033

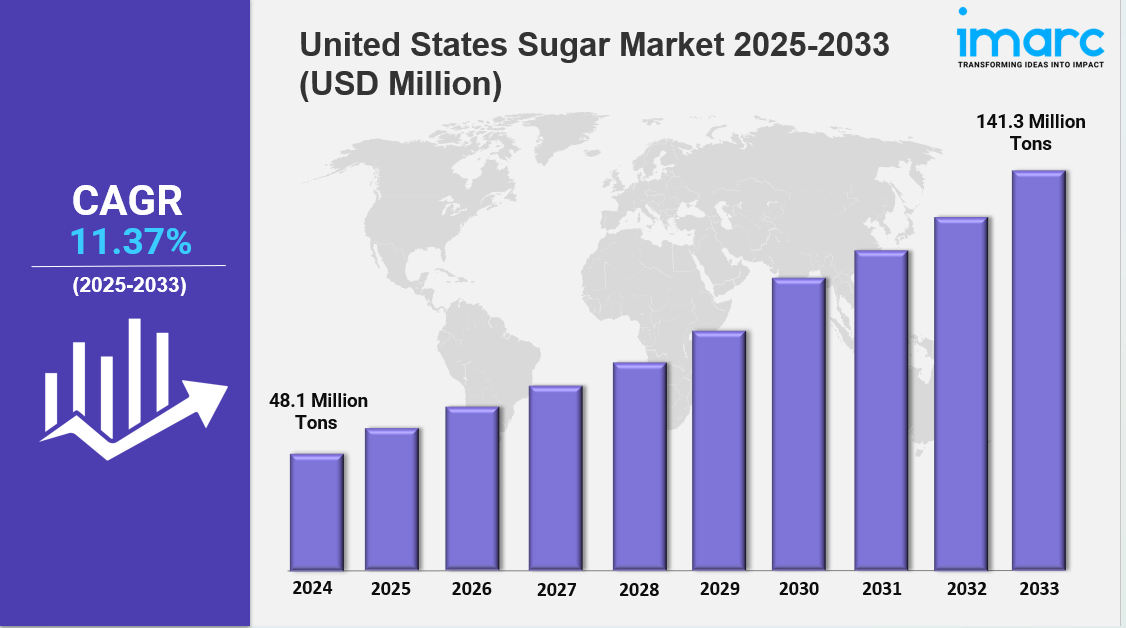

United States sugar market size reached 48.1 Million Tons in 2024. Looking forward, IMARC Group expects the market to reach 141.3 Million Tons by 2033, exhibiting a growth rate (CAGR) of 11.37% during 2025-2033. The U.S. market is expanding due to rising demand for convenient sweeteners, robust food and beverage production, and growth in industrial applications. Growth is driven by flavored and brown sugar trends, health-conscious product lines, and strong processing infrastructure, making it dynamic and competitive.

Key Market Highlights:

✔️ Steady market growth driven by sustained demand from food and beverage manufacturing sectors

✔️ Increasing focus on alternative and low-calorie sweeteners amid rising health awareness

✔️ Expanding domestic production supported by technological advancements in sugar processing and crop yields

Request for a sample copy of the report: https://www.imarcgroup.com/united-states-sugar-market/requestsample

United States Sugar Market Trends and Drivers:

The United States sugar market is undergoing significant structural changes driven by shifting consumer preferences, evolving regulatory frameworks, and growing attention to health and sustainability. Public health concerns—particularly regarding obesity, diabetes, and high sugar intake—have contributed to changing purchasing behaviors, reshaping core United States sugar market trends. Major food and beverage companies such as Coca-Cola and PepsiCo have expanded their zero-sugar and reformulated product portfolios, which have increased by over 40% in recent years.

Concurrently, initiatives such as the FDA’s added sugar labeling requirements and localized soda taxes continue to suppress traditional sugar consumption. Alternative sweeteners like stevia and monk fruit now account for approximately 18% of the United States sugar market, reflecting growing consumer demand for low- and no-calorie alternatives. Although sugar use surged briefly during the pandemic due to home baking, the broader United States sugar market outlook remains oriented toward moderation and substitution.

International trade policies are also exerting considerable influence on the United States sugar market outlook. The tariff-rate quota (TRQ) system maintains elevated domestic sugar prices, shielding U.S. producers but generating friction with food manufacturers seeking lower input costs. Trade limitations with Mexico—formerly the top sugar exporter to the United States—have resulted in tighter supply conditions, further compounded by Brazil’s ethanol-first export strategy and climate-related disruptions in regions like Louisiana. These pressures are prompting increased calls for TRQ reform and diversification of supply chains to mitigate the impact of inflation and volatility.

Sustainability is becoming a defining feature of United States sugar market trends. Companies such as Florida Crystals have adopted regenerative agriculture, achieving annual carbon reductions exceeding 120,000 tons. Sugar beet growers are incorporating precision farming technologies to enhance water efficiency and reduce chemical dependency. Meanwhile, rising scrutiny over labor practices has accelerated adoption of certified Fair Trade sugar, which now represents 18% of retail sugar sales. Retailers are placing increased demands on suppliers to meet environmental, social, and governance (ESG) criteria, encouraging operational changes and contributing to industry consolidation.

The competitive structure of the United States sugar market continues to consolidate. The top five sugar cooperatives now control over 63% of beet processing and more than 70% of cane refining capacity. Since 2020, investments exceeding $2 billion have focused on automation and capacity upgrades. Contract farming has become the predominant supply model, offering processors stability while limiting the role of independent growers. Industrial buyers—led by beverage and confectionery producers—account for roughly 68% of U.S. sugar consumption. However, demand growth in this segment has decelerated to 0.8% annually, primarily due to reformulations.

Niche categories such as organic and non-GMO sugar are growing at a projected CAGR of 7.2%, further supporting United States sugar market trends toward health-conscious and clean-label consumption. Government policy continues to shape the United States sugar market outlook. Federal sugar support programs—estimated at $3.5 billion annually—remain central to Farm Bill negotiations. Ethanol subsidies are influencing market dynamics by redirecting sugarcane toward fuel production. Technological adoption is rising; approximately 40% of U.S. sugar mills now use blockchain and traceability systems to meet ESG reporting requirements.

Climate disruptions, including the 2024 Panama Canal drought, have stressed supply chains and elevated spot market prices by over 20%. In response, gene-edited, drought-tolerant sugar beet strains are now in early-stage commercialization to stabilize long-term output. Looking forward, the United States sugar market outlook will be defined by a complex interplay of health priorities, sustainability initiatives, and agricultural protections. Companies that focus on innovation, traceability, and flexible sourcing strategies are best positioned to increase their United States sugar market share amid continued transformation. As both regulatory scrutiny and consumer expectations rise, the future of sugar in the U.S. will be determined by its ability to meet increasingly multidimensional demands.

United States Sugar Market Segmentation:

The market report segments the market based on product type, distribution channel, and region:

Study Period:

Base Year: 2024

Historical Year: 2019-2024

Forecast Year: 2025-2033

Breakup by Product Type:

- White Sugar

- Brown Sugar

- Liquid Sugar

Breakup by Form:

- Granulated Sugar

- Powdered Sugar

- Syrup Sugar

Breakup by Source:

- Sugarcane

- Sugar Beet

Breakup by End User:

- Food and Beverages

- Pharma and Personal Care

- Household

Breakup by Region:

- Northeast

- Midwest

- South

- West

Competitive Landscape:

The market research report offers an in-depth analysis of the competitive landscape, covering market structure, key player positioning, top winning strategies, a competitive dashboard, and a company evaluation quadrant. Additionally, detailed profiles of all major companies are included.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145