India Hydraulic Fracturing Market Size, Share, Trends, Industry Analysis, Report 2025-2033

Market Overview 2025-2033

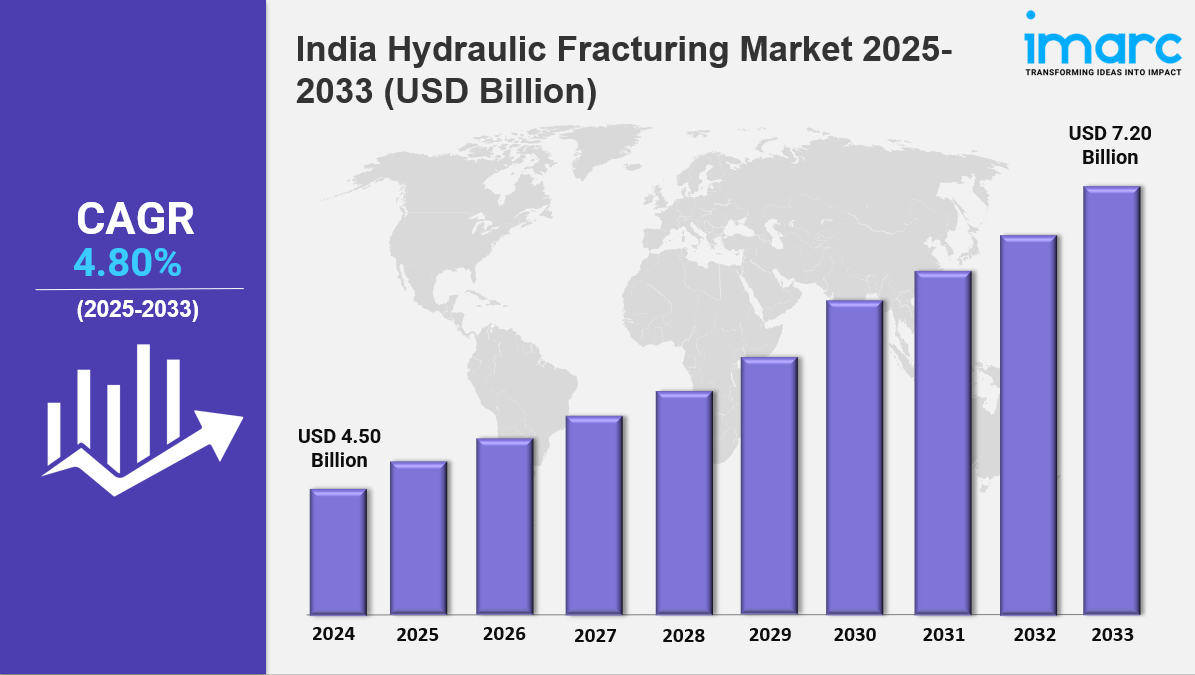

The India hydraulic fracturing market size reached USD 4.50 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 7.20 Billion by 2033, exhibiting a growth rate (CAGR) of 4.80% during 2025-2033. The market is growing due to increasing energy demand, rising shale gas exploration, and advancements in drilling technologies. Government initiatives, infrastructure development, and sustainability trends are key factors driving industry growth.

Key Market Highlights:

✔️ Strong market growth driven by increasing demand for oil and gas exploration

✔️ Rising adoption of advanced fracturing technologies to enhance extraction efficiency

✔️ Expanding government initiatives supporting energy security and domestic hydrocarbon production

Request for a sample copy of the report: https://www.imarcgroup.com/india-hydraulic-fracturing-market/requestsample

India Hydraulic Fracturing Market Trends and Drivers:

India’s escalating energy consumption, driven by rapid industrialization and urbanization, has intensified the focus on unconventional energy sources like shale gas. The India hydraulic fracturing market is emerging as a crucial segment, utilizing advanced technologies to unlock trapped hydrocarbons in complex geological formations, particularly in the Cambay, Krishna-Godavari, and Cauvery basins. The government’s push to reduce import dependency and achieve energy security has led to strategic partnerships with global oilfield service companies, fostering technical expertise and infrastructure development.

In 2024, state-owned enterprises like ONGC and Reliance Industries allocated substantial investments to accelerate shale gas exploration, aiming to enhance the India hydraulic fracturing market share and increase domestic natural gas production by 30% by 2030. However, water scarcity and land acquisition challenges in drought-prone regions like Rajasthan and Gujarat pose significant hurdles, driving innovations in water-efficient fracturing fluids and community engagement strategies.

Environmental concerns over groundwater contamination and seismic risks have prompted stringent regulatory oversight, reshaping India hydraulic fracturing market growth dynamics. The Ministry of Environment’s 2024 amendment to the Hydraulic Fracturing Policy mandates comprehensive environmental impact assessments (EIAs) and real-time monitoring of wastewater disposal, increasing operational costs by 15–20%. Public opposition, particularly in agrarian states like Punjab and Maharashtra, has delayed project approvals, pushing companies to adopt greener technologies such as recycled water systems and bio-based fracturing chemicals.

The cement and steel industries are responsible for 40% of the market’s growth through captive shale gas consumption, indicating that demand is still high in energy-intensive industrial corridors despite these obstacles. The hydraulic fracturing industry in India is undergoing a transformation thanks to the use of automated drilling rigs and AI-driven fracture modeling. In order to increase recovery rates by 25%, companies such as Schlumberger and Halliburton are collaborating with regional players to implement machine learning algorithms that optimize fracture geometry and well placement. In line with India’s net-zero pledges, the deployment of hybrid fracturing fleets in 2024—powered by solar energy and LNG—reduced carbon emissions by 30%.

Meanwhile, cost-saving measures, such as localized proppant manufacturing and modular well designs, have cut per-well expenses by $1.2 million, attracting mid-sized exploration firms and boosting India hydraulic fracturing market growth. The India hydraulic fracturing market is navigating a transformative phase, balancing energy security imperatives with sustainability mandates. A key trend is the integration of digital twins and IoT sensors to enhance operational transparency, enabling regulators and firms to monitor reservoir performance and emissions in real time. The market is also witnessing a shift toward “fracking-light” techniques, such as cyclic gas injection and nitrogen foam fracturing, which minimize water usage and environmental disruption.

A 50% increase in R&D investments was brought about by the government’s introduction of tax incentives for low-carbon fracturing technology in 2024, which marked a turning point halfway through the decade. Nonetheless, shale gas economics are still under pressure from LNG imports and renewable energy initiatives, with analysts predicting a 6–8% annual growth rate through 2030. The next stage of market evolution is anticipated to be dominated by strategic partnerships between international IT suppliers and Indian E&P businesses, with an emphasis on scalable, environmentally friendly solutions.

India Hydraulic Fracturing Market Segmentation:

The report segments the market based on product type, distribution channel, and region:

Study Period:

Base Year: 2024

Historical Year: 2019-2024

Forecast Year: 2025-2033

Breakup by Well Type:

- Horizontal

- Vertical

Breakup by Fluid Type:

- Slick Water-based Fluid

- Foam-based Fluid

- Gelled Oil-based Fluid

- Others

Breakup by Technology:

- Plug and Perf

- Sliding Sleeve

Breakup by Application:

- Shale Gas

- Tight Oil

- Tight Gas

Breakup by Region:

- North India

- South India

- East India

- West India

Competitive Landscape:

The market research report offers an in-depth analysis of the competitive landscape, covering market structure, key player positioning, top winning strategies, a competitive dashboard, and a company evaluation quadrant. Additionally, detailed profiles of all major companies are included.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145